PRELIMINARY PERFORMANCE REVIEW OF THE

PUBLIC EMPLOYEES INSURANCE AGENCY

FINANCE BOARD

The Cost of Insurance Plans

are not Equitably Apportioned

Among Participants

The PEIA Finance Board Actively

Participates

in Meetings

Issue Area 1: The Cost of Insurance Plans are not Equitably Apportioned Among Participants.

The four groups involved with PEIA's insurance plans are State and local

employers, State and local employees and retirees, and health care providers.

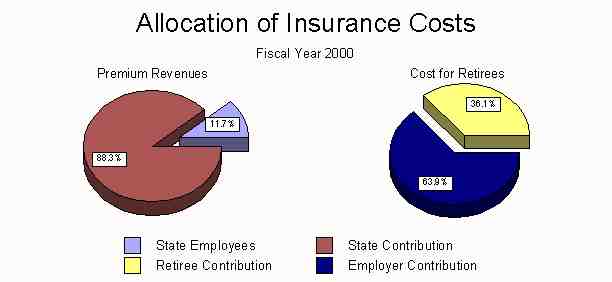

The total cost of PEIA's insurance plans for the year 2000 is nearly $350

million. Between 88% and 93% of the plan costs for State employees are

paid for by the State (See Figure 1). It is not known what percent

local government employers pay for the premiums of local government employees,

because each local government agency determines its employee's portion.

Therefore, local employees may pay a larger or smaller percentage of their

premiums than State employees. State and local employers also contribute

funds for the costs of State and local retirees by paying premiums in excess

of the amount necessary for their active employees. The contribution rate

for retirees is between 60% and 70% of the retirees' insurance costs. This

employer contribution for retirees is growing three times faster than the

growth of employers' total contributions for both retirees and employees.

In addition to PEIA plan costs, there are also costs incurred by providers

in the form of contractual allowances that pay providers less than

their actual costs. The effect is that PEIA contributes to the financial

stress that health care providers are under by having them bear a portion

of the costs.

Chapter 5, Article 16, Section 5 of the West Virginia State Code states

in part:

(a) The purpose of the finance board created by this article is to bring fiscal stability to the public employees insurance agency through development of annual financial plans and long-range plans designed to meet the agency's estimated total financial requirements, taking into account all revenues projected to be made available to the agency, and apportioning necessary costs equitably among participating employers, employees and retired employees and providers of health care services.(Emphasis Added)

Necessary costs are the agency's administrative costs, participant's claims for both medical and prescription drugs, life insurance and managed care costs. Although all costs inherent with this agency are necessary and materially important, the costs for medical and prescription drug claims are the costs which create the largest disparity among participants.

The PEIA Finance Board obtains funding to pay these costs by setting premium rates for the employers, employees and retirees. These rates are set based on a variety of factors including the amount available from the state budget for the employers' share. In addition to premiums, the Finance Board sets allowable charges or reimbursement amounts for providers. This is how the providers indirectly pay their share of plan costs. The providers' share will be explained further in a later section.

Employer, Employee and

Retiree Costs

Over the past 8 years of actuarial reports

it can be determined that these costs are in fact being paid on a disproportionate

basis. The employer has absorbed the large majority of costs created by

employees and retirees. This is identifiable in the actuarial report and

in the percentages paid by the employer for a covered single employee or

family which is 96% and 90% respectively. Per information gathered by The

Segal Company in a report prepared for the WV Legislature, the single percentage

of 96% is 9% above the national average of 87%, with the family percentage

being 16% above the national average of 74%.

Even though employees have had premium increases, the employer still pays a large percentage in comparison with other state plans. Based on information from the National Association of State Budget Officers, West Virginia ranked sixth in the nation in percentage of total funds allocated to state insurance plans in fiscal year 1997. Appendix B details the percentage increases per various participants' premiums over the past 10 years. Based on PEIA numbers for fiscal years 1997 through 1999, employer premiums have risen $35 million. This increase in premiums doesn't even take into account further funding by the Legislature in fiscal years 1998 and 1999 totaling $7.1 million to avoid increases in policyholder deductibles.

Retiree Funding

West Virginia state retirees have always

been eligible for continued health coverage in PEIA. Due to the age of

retirees, they generally require more medical treatment. This placed the

Finance Board in a position of either requiring retirees to fund their

own expenses or use a portion of employers' total premium contributions

to make up the difference between the retirees' contributions and their

total claim expenses and administrative costs. The latter choice was made.

This means any expenses incurred by retirees in excess of their premiums

will be paid by the State and local employers. Therefore, employers are

billed by PEIA in excess of the amount necessary for their active employees

to compensate for the insufficient retiree premium. The State has paid

an average of 65% of total claim expenses and administrative costs for

retirees over the past 8 years. As exhibited in Table 1, you can see the

difference and the amount contributed by employer funds for retirees.

| Table 1

Employers' Contribution Rates and Amounts for Retirees |

||

|

Fiscal Year |

Employers'

Contribution Rates |

Employers'

Contribution Amount |

| 1993 | 60% | $34,040,000 |

| 1994 | 64% | $39,457,000 |

| 1995 | 67% | $46,176,000 |

| 1996 | 67% | $44,920,000 |

| 1997 | 70% | $53,744,000 |

| 1998 | 65% | $51,106,000 |

| 1999 | 65% | $57,962,000 |

| 2000 | 64% | $55,821,766 |

--Employer Contribution Amount is calculated by taking the retiree's share of the plan costs and subtracting their premiums. For FY 1993, the retirees plan costs were 56,659,000 and their premiums were 22,619,000.

22,619,000 (premium revenue) - 56,659,000 (plan costs) = -34,040,000 (costs picked up by employers)

--Employer Contribution Rates are calculated by taking the retiree fund negative balance and dividing it by the plan costs (-34,040,000(negative fund balance)/56,659,000(retiree plan costs) = 60%).

A concern with the retiree fund is the

rate of growth of the needed employer contributions compared to the rate

of growth in the amount of employers' contributions for both employees

and retirees (see Table 2). Since 1993 to 2000, the needed retiree contribution

from employers has increased by 64%, while the total employer contribution

for both employees and retirees has increase by only 20% over the same

period. While retirees' total expenses have been rising 64%, retiree premiums

have in many years not changed at all because the Board has relied on Employers

to pay the difference. The disparity in growth rates creates the situation

that: 1) employers will be under pressure to pay a larger proportion of

its premiums for retirees; 2) If employers cannot pay the larger proportion,

then the growth in the needed retiree contribution absorbs the Board's

ability to accumulate surpluses or reserves for unexpected events or forecasting

errors.

|

Growth Rate of Employers' Contribution to Retirees & the State Employer's Contributions for both Active Employees and Retirees |

||||

|

Fiscal Year |

Employers' Contribution to Retiree Costs |

Percentage Increase |

State Contributions for Active Employees & Retirees |

Percentage Increase |

| 1993 | $34 million | $232.5 million | ||

| 2000 | $55.8 million | 64% | $279.7 million | 20% |

Providers

Providers make up all health care facilities

that provide services to policyholders. Although they do not literally

contribute premium revenues to PEIA, they do, however, pay in an indirect

manner. This is accomplished by PEIA setting reimbursement rates for particular

procedures performed by the provider. For example, when a patient receives

a physical, the provider is paid what PEIA's reimbursement rate is for

a physical regardless what the provider bills. Also, due to the fact that

health care providers cannot "balance bill" patients in West Virginia;

providers must accept, to a certain extent, the reimbursement rates set

by PEIA. It should also be noted that PEIA's policyholders make up approximately

11% of the State's population which adds to PEIA's market power within

the State and bordering State counties.

Over the past 10 years multiple cost saving measures have been enforced by the PEIA on providers. This has been accomplished by reducing physician fee schedule reimbursement, hospital fee schedule reimbursement and implementing resource-based relative value scale. PEIA has provided dollar estimates showing a $47,188,000 reduction in revenues to providers based on changes to the plan over the past 10 years.

These data are supported by the West Virginia

Health Care Authority annual reports to the Legislature. The reports show

that contractual allowances for government insurance programs are a contributing

factor for lower hospital profit margins. Medicare, which represents 50%

of inpatients in the State, paid 92 cents for each $1 of operating expenses

(net bad debt, charity care and contractual allowances) during fiscal year

1999. While Medicaid, which represented 16% of inpatients in the state,

only paid 90 cents for each $1 of costs (net bad debt, charity care and

contractual allowances). The contractual allowance for Medicare reduced

gross revenues by $938,280,685 and Medicaid's allowances reduced gross

revenues by $270,673,610. PEIA's contractual allowances reduced providers'

gross revenues by $73,226,507 and paid 98 cents to each dollar of expenses

(net bad debt, charity care and contractual allowances) during fiscal year

1999. Table 3 below displays the contractual allowances of each government

insurance provider.

| Table 3

Government Insurance Contractual Allowances for All Hospitals FY 1999 |

|||

| Gross

Patient Revenue |

Contractual Allowances | Net

Patient Revenue |

|

| PEIA | $173,792,404 | $73,226,507 | $100,565,897 |

| Medicare | $2,087,956,713 | $938,280,685 | $1,149,676,028 |

| Medicaid | $620,307,115 | $270,673,610 | $349,633,505 |

| Source: West Virginia Health Care Authority Annual Report, 2000, P. 30. | |||

As can be seen by these numbers, PEIA pays

more per dollar and shows a lower contractual allowance than Medicare or

Medicaid. But with the three governmental programs combined, providers

may not be able to assume further reductions, and an accessibility problem

could arise. The possibility of provider accessibility limitations could

occur with continued reimbursement rate decreases.

Conclusion

The PEIA Finance Board has relied upon

the employer and providers to pay an inequitable amount of rising plan

costs. This is largely due to shortfalls of retiree and employee premiums

in relation to each groups' costs. The Finance Board has not set rates

representative of the inflationary costs for employees and retirees. A

quote from the "Segal Report - Legislative Study" is as follows:

The State appears to have gone out of its

way to absorb the majority of inflationary cost increases in the PEIA program

without passing along to employees and retirees their fair share of those

increases. As a result, the premiums charged to employees and retirees

are among the lowest of all states.

The providers have also been used to absorb

the inflationary medical costs by reducing reimbursement rates. This is

done rather than increasing employee, employer and retiree premiums. But,

there is concern of reaching the limit in reducing provider cost reimbursement

further without an adverse effect on the provider industry and accessibility

of health care.

Recommendation 1:

The PEIA Finance Board should implement tools provided in the Code which allow them to set premiums based on individual participant group costs and ability to pay for all participants. The Finance Board should implement an ability to pay premium schedule for retirees in addition to years of service. Information is obtained by the Agency for premium assistance programs and could be used at the other end of the spectrum for increased premiums due to income.

Recommendation 2:

The PEIA Finance Board should implement premium establishment methods which offset medical cost inflation. A formula should be developed which considers each participant groups' costs to the plan, medical cost inflation rates, and other necessary factors to determine premiums for each participant group. In addition, the Finance Board needs to determine and set the percentages expected from each participant so less ambiguity surrounds the budget process. Once this is determined, all participants' costs should then be adjusted representative of medical cost increases on a percentage basis.

Recommendation 3:

The PEIA Finance Board should continue

their method of controlling provider costs with reimbursement rates but

maintain close scrutiny of these methods to avoid harming providers.

Issue Area 2: The PEIA

Finance Board Actively Participates in Meetings.

The intent of the Public Employees Insurance Agency (PEIA) Finance Board is to develop financial plans that provide financial stability to PEIA' s insurance programs. In developing these plans, it is also the intention to have citizen input representing a variety of interest groups, including a representative of education employees, a representative of public employees, a representative of organized labor and three members from the public at large. The citizen members take their responsibility seriously through providing adequate input in financial plan development and maintaining close to perfect attendance.

Board Members Provide

Adequate Input in Developing Financial Plans

A Board that consists of citizen members

and the Director of the administrative agency runs the risk of having most

of the decision making done by the Director and plans being implemented

without Board approval. Therefore, part of this review included an assessment

of the citizen members' involvement in developing the financial plans.

A review of the Board minutes indicates that Board members take their responsibilities

seriously as indicated by the high number of meetings and near-perfect

attendance since 1990 (see Table 4).

| Table

4

Meetings and Attendance |

|||

| Year | Number of Meetings | Quorum | Attendance Rate |

| 1990 | 17 | 17 | 100% |

| 1991 | 17 | 17 | 91% |

| 1992 | 9 | 9 | 98% |

| 1993 | 5 | 5 | 92% |

| 1994 | 7 | 7 | 97% |

| 1995 | 12 | 12 | 97% |

| 1996 | 11 | 11 | 85% |

| 1997 | 13 | 13 | 94% |

| 1998 | 13 | 13 | 92% |

| 1999 | 8 | 8 | 82% |

| March, 2000 | 1 | 1 | 100% |

West Virginia Code §5-16-5 states that the Finance Board shall meet on at least a quarterly basis. The Finance Board has met well in excess of the required quarterly meetings for the past 10 years. From 1990 through March 2000, the Finance Board has held 113 meetings, for an average of 11 meetings per year. The Board attendance rate was 93% for this duration. Consequently, a quorum has always been reached.

Board minutes also reveal that members actively participate in meetings. The members submit a variety of requests to PEIA staff and the Actuary to be introduced for the development of financial plans including:

Conclusion

PEIA Finance Board members are actively

involved in developing and carrying out financial plans. The members are

in compliance with the statute by maintaining close to perfect attendance,

meeting quarterly and with a quorum present. Additionally, the Board members

actively take part in developing, approving and implementing plans.

Recommendation 4:

The Board members should continue to

attend meetings and actively participate in the development, approval and

implementation of financial plans in order to attempt to keep financial

stability within PEIA.